Three-quarters of respondents to our latest survey1 expect their companies to enjoy a profit increase in the next year, and fewer than half expect to cut costs during the same period—both firsts since October 2008, when we began asking. On the whole, this survey shows that executives see economies on the mend, with positive prospects for their countries—84 percent expect national GDP to rise in 2010—as well as for their companies.

But the results also show uncertainty and uneasiness about the future, particularly at the global level. When asked about the likeliest description of the global economy over the next three months, 46 percent of executives pick “constrained global markets perpetuate imbalances”—far more than choose any other description. This view, along with a dip in the share of respondents who expect their national economies to be better in six months, implies a slight dampening of economic hopes since December. Low consumer demand is seen as the largest single threat to national economic recovery in developed economies.

Respondents in developing economies, however, see a bright picture for both their companies and national economies. Further, they identify very different threats to growth: most notably, high commodity prices and currency values.

Better days . . .

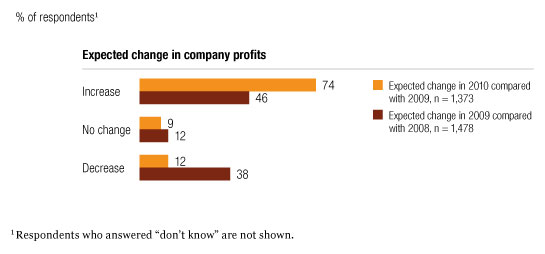

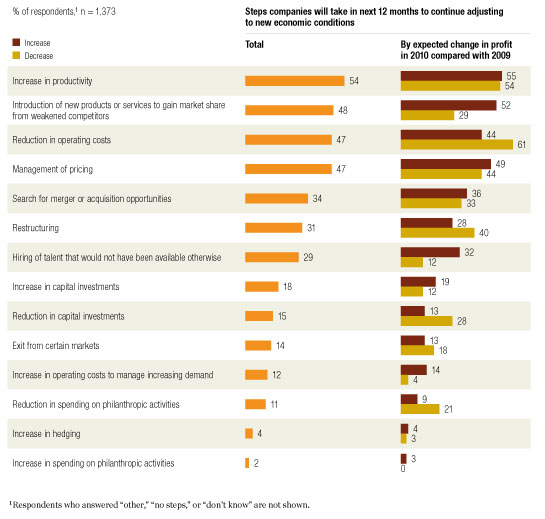

The results indicate that companies are continuing to make progress in managing successfully in the wake of the severe economic crisis. The share of executives expecting a rise in profits in the current year is strikingly higher for 2010 than it was in December 2009: 74 percent versus only 46 percent, respectively (Exhibit 1). What’s more, although corporate cost cuts are continuing to make the news, many respondents seem to expect higher profit to come from successful sales rather than cuts alone. Indeed, among executives who expect their companies’ profits to rise, 60 percent also expect a rise in customer demand; they also report a greater focus on sales-related tactics than do executives at other companies. Executives at these companies are likelier than others to say they will be introducing new products or services and managing pricing over the next 12 months, while cost cutting is a less likely tactic (Exhibit 2).

That fewer than half expect to continue cutting costs is particularly interesting in light of another finding: only about a third of respondents expect the cuts they’ve already made to be sustained over the next 12 to 18 months. This expectation, too, may well indicate hopes for renewed growth.

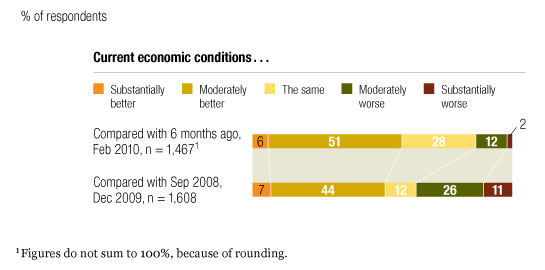

At the national level, the share of respondents expecting GDP to rise in the currentyear also has grown markedly since December 2009, from 57 percent to 84 percent. More executives are also positive about their countries’ current condition (Exhibit 3).

Expecting higher profits in 2010

How to deal with a new economy

Better economic conditions

. . . but wariness too

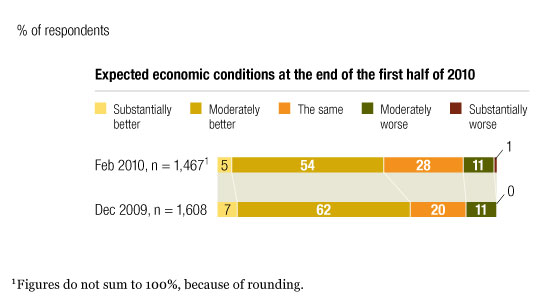

However, on some other measures, this optimism is tempered and has declined slightly since December. The share expecting economic conditions to be “substantially” or “moderately better” at the national level at the end of June 2010, for example, has fallen to 59 percent, from 69 percent (Exhibit 4).

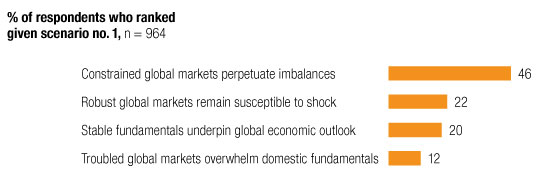

Further, responses to a set of potential scenarios for the future of the global economy indicate significant wariness.2 Nearly half expect that a future in which “constrained global markets perpetuate imbalances” is the likeliest scenario over the next three months (Exhibit 5). Among other elements, this scenario anticipates strength in emerging markets but a failure to repair fundamental economic policies and a weak US consumer sector. This finding is consistent with the view that low consumer demand is the single biggest threat to growth, which is particularly strong among respondents in developed economies; 53 percent of respondents overall say so, and the figures rise to 57 percent in North America and 60 percent in Europe.

Tempered optimism

Concern about global imbalances

A different story in emerging markets

For respondents in emerging markets, this scenario offers more good news than bad. Consistently, respondents in these markets are much likelier than others to expect increases in profits, customer demand, and even workforce size. These executives also are likelier than others to be positive about a continued resurgence at the national level, with 73 percent expecting better conditions by the end of the first half of 2010 (Exhibit 6).

Respondents in emerging markets are also far less worried than others about low consumer demand braking their countries’ economic growth. The most frequent concern for those in India, chosen by 63 percent, is high commodity prices. Indeed, majorities of respondents in India expect higher prices on four of the five commodities we asked about (gold, iron ore, oil, and wheat); those shares are generally far higher than they are for executives in other regions. In other developing markets, meanwhile, the largest concern is currency values, chosen by 44 percent. This is consistent with findings from our December 2009 survey showing that, for respondents in emerging economies, movements in exchange rates in many cases had a greater effect on profits, market share, and strategic decisions making than they did in other geographic markets.

Strength in emerging markets