A gloomy economic stasis has taken hold, responses to a McKinsey Quarterly survey—in the field from March 10, 2009, through March 16, 2009—indicate.1 The percentage of the executives who say economic conditions have gotten worse at the national level hasn’t increased, but fewer than a third expect an upturn this year.

Executives overall are confident with how their companies are managing the crisis, though 53 percent expect profits to drop in the first half of 2009, and the number expecting to shed workers has jumped eight percentage points in six weeks. Companies that executives describe as well managed are likelier than others to be reducing both operating costs and capital spending—and perhaps not weakening operations a great deal, because these companies are also likelier than others to be improving productivity. Overall, the results show that most companies are not actively seeking more cash.

This survey also solicited executives’ views on some topics of intense public debate. Respondents think “bad banks” are a good idea, disagree on whether CEOs are paid too much, and overwhelmingly say the public trusts business less than it did before the crisis—and lay the blame at the doors of financial firms.

Big questions

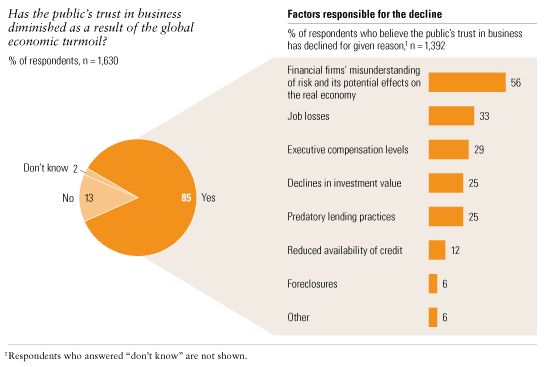

Among the respondents’ views, there is no ambiguity about whether trust in business has fallen as a result of the crisis: 85 percent say it has and—by a wide margin—they blame the decline mostly on financial firms’ misunderstanding of risk (Exhibit 1). That response holds even among executives at financial firms. Among respondents who selected “other,” many specified “greed.”

There is much less consensus among the respondents on whether CEO compensation is excessive in their industries: 43 percent say it is, and 47 percent say it isn’t.2 Perhaps not surprising, nearly 60 percent of respondents in finance say yes, as do 49 percent of respondents at very large companies (those with annual revenue of $1 billion or more).

Another area of intense public debate is how to restore liquidity and stability to markets. One option is for governments to buy the financial institutions’ toxic assets and consolidate them into a “bad bank” to restore liquidity to the rest of the system (a plan similar to what the US government proposed on March 23, 2009). Fifty-four percent of all respondents—and 61 percent of those in financial services—say creating a bad bank would help restore liquidity. Executives across Asia are likeliest to hold this view.

The risks of poor judgment

When we asked respondents which one action would do most to restore market stability, the responses express a clear focus on liquidity, with various ways to achieve it. The paths mentioned by many respondents are lowering taxes for businesses, consumers, or both; increasing consumer confidence and spending; focusing on global responses in regulation, currency management, and confidence building (what one executive calls “sincere cooperation of all nations”); and cogent, long-term leadership, described by another respondent as “pick a plan, stick with it, communicate tactics, be clear.” Respondents also call for government actions of all sorts, as well as the reverse: “Leave the banks and companies alone. Let the bad fail and the good will thrive—this will set our globe back into balance.” Perhaps the most hopeful note comes from an executive who writes, “Have patience. Confidence and risk tolerance will improve naturally, as it is part of human nature.”

Stasis, with a few signs of hope

Patience will indeed be needed. Overall, executives say their national economies are in very poor shape—almost 90 percent say conditions have declined since September 2008—but haven’t gotten worse in the past six weeks. Similarly, the proportion of respondents expecting their nations’ GDPs to drop stands at three-quarters, as it did six weeks ago. The proportion of executives expecting an economic upturn this year has dropped from 40 percent to 30 percent, suggesting that respondents expect the current situation to continue for some time.

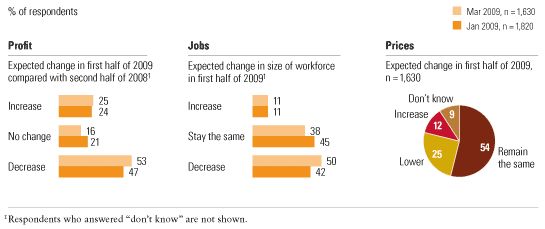

Executives’ responses about their companies indicate that, over the past six weeks, they have settled into the expectation that poor conditions will continue for some time. Half of all respondents expect their companies to shed workers in the first half of 2009—an eight-percentage-point increase from just six weeks ago, when more expected an upturn to occur this year (Exhibit 2). And more respondents to this survey than to earlier ones offer a prediction for their companies’ near-term profits: 53 percent expect profits to be lower in the first half of 2009 than in the second half of 2008, and these are mostly the same respondents who expect their companies to shed workers. Only 6 percent are unsure.3 Finally, the executives’ expectations about how the crisis will change their industries haven’t shifted notably since November 2008. Roughly two-thirds expect lower growth, and as in November smaller percentages expect consolidation and a lower tolerance of risk.

Expecting to shrink

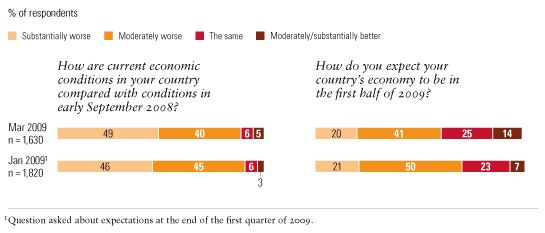

Although only 14 percent of respondents expect their countries’ economic conditions to improve in the first half of 2009, that’s more than twice the percentage that, six weeks ago, expected an improvement (Exhibit 3). The proportion of hopeful executives has increased most in Europe and North America.

More hopeful than in January

Further, most companies’ finances still aren’t on the edge, according to these respondents. Only a minority say their companies are seeking external funding (as has been the case since we began asking, in October 2008). More companies are seeking funds for new initiatives than for any other purpose (Exhibit 4). These responses indicate that growth is still on the agendas of some companies, particularly in high tech and telecommunications. Among the other reasons for seeking funds, increasing available cash has decreased in importance since December.4

New funds for new initiatives

Our findings may suggest that although some companies are having trouble meeting everyday expenses, most companies are less focused on building a large pool of ready cash than they were a few months ago. Since interest payments regularly cut into cash, that conclusion may be supported by the finding that only 39 percent of all respondents say that their companies have actively sought to decrease debt since last September (though 16 percent of the respondents don’t know). There are some differences by region and industry, but only in manufacturing do a majority of respondents—a bare 51 percent—say that their companies have sought to reduce their debt.

It must be noted that over the past six weeks, the number of companies seeking funds has jumped to 30 percent, from 24 percent—the first big change since October. The increase comes from financial companies and from companies in Europe and in Latin America and other developing economies.

Companies doing more with less

More than half of all respondents—57 percent—say that because of good management, their companies have been less hurt than most by the crisis. Although that figure probably indicates hope for better results than are entirely plausible, it also indicates a confidence in management that runs counter to many other reports. Indeed, even at companies where executives expect profits to drop in the first half of 2009, 51 percent say that their companies have been well managed, along with 52 percent of executives at financial firms.

Perhaps even more interesting, companies that (according to their executives) are well managed have a focus somewhat different from the one that executives at poorly managed companies support (Exhibit 5). Well-managed companies have a much stronger emphasis on reducing both operating costs and capital spending, as well as on improving productivity. Although executives at poorly managed companies also advocate cutting operating costs, they then turn to restructuring and hiring.

Well-managed companies target costs and productivity

Little action in the capital markets

Given the precipitous decline in stock prices in the past year, it is notable that just over half of all respondents say that their companies have taken no action in the capital markets as a result of the crisis (Exhibit 6). Although the percentage drops among public companies, it’s still a remarkably high 30 percent. And when a company does act, the most frequent response is to support its stock through better communication rather than to buy its stock or stakes in other companies.

On the sidelines of the capital markets