Executives’ expectations for the global economy, their national economies, and their companies’ prospects have taken a huge hit in the past three months. Our latest survey1 finds most notably that only 18 percent of executives in the eurozone expect near-term improvement in their national economies (compared with 29 percent of all respondents, down from 48 percent in June). Most executives think a double-dip recession will hit advanced economies over the next six months, and nearly three-quarters say there is at least some chance of the eurozone splintering within the next two years.

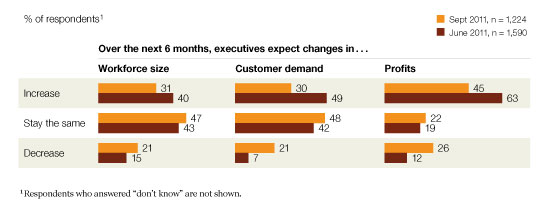

The gloom has spread to the company level as well: executives’ views on corporate performance over the next six months have fallen, after remaining fairly stable through the spring. The shares of executives who expect customer demand or the size of their companies’ workforce to rise have both fallen below a third, and the share expecting an increase in profits in 2011 has fallen to 45 percent, from 63 percent in June.

Finally, though respondents in emerging markets are only slightly more hopeful about the global economy than those in other regions, they are notably more hopeful about their own economies, as well as their companies’ prospects—indeed, 52 percent expect corporate profits to improve in the rest of this year, compared with 43 percent of respondents in developed economies.

Quantifying global turmoil

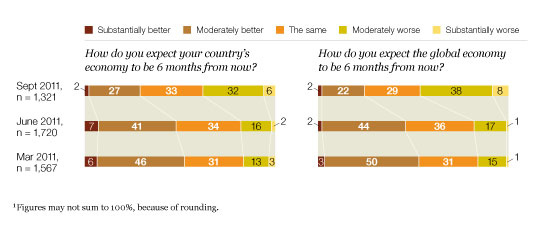

The shares of survey respondents expecting their home economies and the global economy to worsen over the next six months has more than doubled since June (Exhibit 1). That’s consistent with the finding that most executives expect a double-dip recession in advanced economies over the next six months: only 15 percent say there’s a 10 percent or less chance of one.2 More are also saying there is some likelihood that the eurozone will split in two years, up to 73 percent, from 57 percent in June. Indeed, of four future economic scenarios, the share saying that stalled globalization—a lack of robust growth in both developed and emerging markets—is likeliest to happen over the next decade jumped 12 percentage points since our previous survey, to 29 percent.3

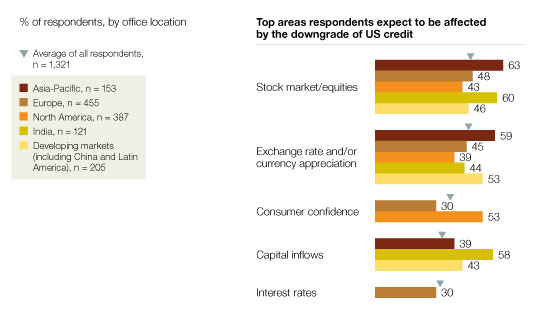

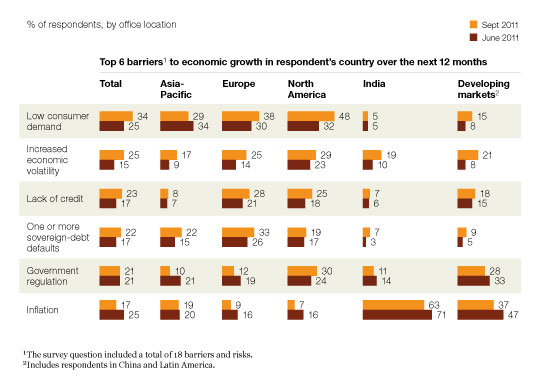

Most respondents expect Standard & Poor’s downgrade of US credit to affect their countries’ economies in some way, though the expected effect varies by region (Exhibit 2). It is certainly not surprising that economic volatility has risen in importance as a major barrier to national economic growth, though even now only a quarter of respondents choose it (Exhibit 3). Fears about unemployment have risen in all regions, while fears about inflation have fallen.4

Economic expectations deteriorate

US downgrade effects are widely felt

More concerns about demand and volatility

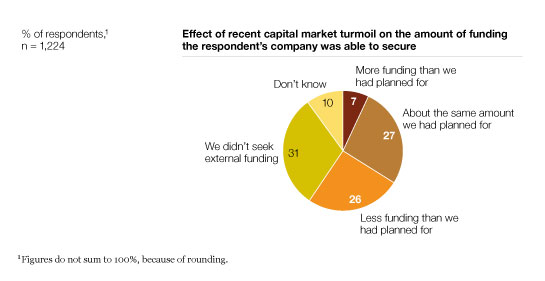

At the company level, overall expectations are down (Exhibit 4), and 61 percent of respondents say that the current turmoil has changed their companies’ strategic or financial plans for the next six months. Yet a fairly small share of respondents say that the external funding their companies secured was less than what they had planned for, because of the capital market turmoil, while a little more than a quarter say funding has gone as planned (Exhibit 5). What’s perhaps most notable is that the 31 percent who say their companies didn’t seek funding is still lower than the share of respondents to our December 2010 survey who answered a comparable question similarly: at that time, 43 percent said their companies hadn’t sought external funding in the past six months, so it appears that the slow return to the markets seen in the first part of 2011 has not been entirely reversed.

Company outlook is negative

Mixed funding results

Developed Asia is relatively positive

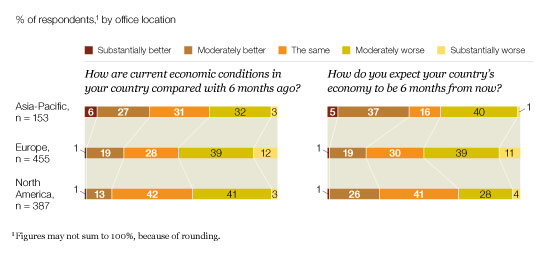

Though the patterns are consistent globally, executives in developed economies report some notable differences about their countries. Thirty-three percent of executives in the developed economies of Asia5 say that economic conditions are better than they were six months ago. This is the same share as in June, while the shares in other regions have dropped substantially for the second survey in a row (Exhibit 6); looking six months out, the picture is much the same.

At the company level, too, executives in developed Asia indicate that their companies are taking a somewhat different approach. At 40 percent, more respondents in developed Asia say their companies haven’t sought external funding than respondents in any other region, and they are by far the likeliest to say their companies are retaining more cash than they were before the summer—49 percent say so, compared with 38 percent of all respondents.6 That tactic may help explain why even though just 22 percent of these respondents expect consumer demand to rise—the lowest share in any region—47 percent still expect profit to rise in the second half of this year.7

In developed Asia, more positive country views

Emerging markets even more so

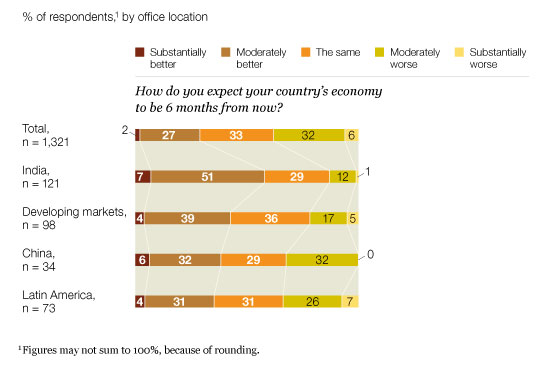

Respondents in China, India, Latin America, and other developing markets are more positive across the board. Higher shares expect improvement in the global economy, and though all respondents’ views on the current economy and near-term expectations have fallen since June, respondents in these countries have a markedly rosier outlook about their national economies’ prospects than their peers in Europe and North America do (Exhibit 7).

Furthermore, executives whose companies do business in these countries seem to share this optimism: wherever their companies are headquartered, those who say higher shares of revenue come from emerging markets also expect higher overall profit.

On the whole, respondents in these regions say their companies’ strategic or financial plans have been affected by the turmoil about as often as respondents in other regions, but smaller shares say their companies are retaining additional cash.8 In most of these countries, slightly higher shares of respondents expect to increase their workforce; the figure rises to 46 percent among respondents in India. Similarly, though their expectations for rising customer demand are lower than in June, they are markedly higher than among executives in developed economies.9 On profit, executives in China and India have higher expectations than those of executives in developed markets: 55 and 63 percent, respectively, expect an increase. The other emerging economies are about the same as in developed markets.

Higher expectations in developing economies