In a survey launched the day after the US presidential election,1 executives from around the world indicate that they expect 2009 to open with a global recession and continuing high volatility in equity markets. They also believe that financial markets will remain more stalled than liquid. And a majority expect their country’s GDP to contract next year—most predict by 2 percent or less.

Nonetheless, many executives say their companies are holding their ground, though some are hard hit. Half of all respondents expect their companies’ profits to stay stable or increase this fiscal year, and some are finding opportunity in turmoil—by entering markets where competitors have weakened, hiring talent that would otherwise not be available, and seeking M&A opportunities. Smaller and private companies generally see themselves in a somewhat better position than larger and public ones. Most companies across the board have not sought external funding since mid-September because they haven’t needed it, and, although few expect to hire in the rest of 2008, only about a third expect to decrease their workforce.

Looking ahead, executives say that governments should take some limited, globally coordinated steps on regulation and fiscal policy, invest in infrastructure, and support a range of industries beyond the financial sector.

Not all companies are desperate

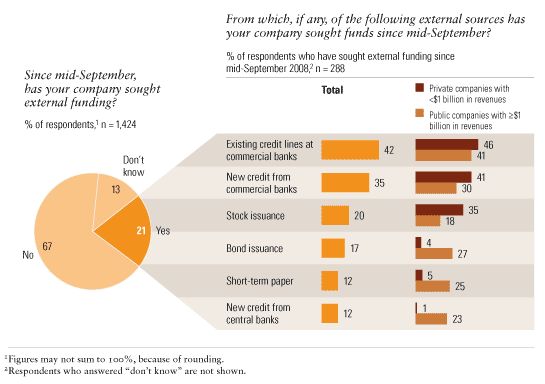

Though the news is filled with reports of companies unable to get the funds they need to operate, two-thirds of respondents to this survey say their companies haven’t sought funds from external sources since mid-September2 —and 81 percent of those say the reason is that their companies don’t need funds. The figures are fairly consistent across regions, industries, and company size and type. Even in the financial services industry, only a third of respondents say their companies have sought funds.

It must be noted that among the relatively small number of companies that did seek funding, the proportion of those that couldn’t get it, 17 percent, has nearly doubled since October, when 9 percent of respondents said they had been unable to obtain funding they had sought in the period from July through September. In addition, 60 per-cent of respondents who have received funding since mid-September say it cost more than it had previously; among those who expect to seek funding during the remainder of 2008, 41 percent expect costs to rise.

It is perhaps not surprising that financial-services firms are having the least trouble securing the funding they seek, given many governments’ support of those firms; larger companies—those with annual revenues of $1 billion or more—and public ones are also slightly more able to get funds than smaller or private ones (74 percent of large companies are also public, 77 percent of smaller companies are also private). This variability may relate to the sources from which companies have sought funding (Exhibit 1).

Sources of funds

Three-quarters of respondents say their company is cutting operating costs in response to the economic turmoil, and 37 percent are cutting capital investments (Exhibit 2). However, some are also finding opportunity—34 percent, for example, are introducing new products or services to gain market share from weakened competitors.

Responding to economic turmoil

A slim majority of executives expect their companies’ workforces to remain stable through the rest of 2008, and 13 percent expect to hire; 35 percent expect their workforces to decrease, an increase of 6 percent from just two months ago (Exhibit 3). There are few regional differences and, not surprising, some large industry differences. Within the next calendar year, slightly more executives expect workforce costs to decrease rather than increase—from 37 percent to 33 percent. In still-growing China and India, more executives expect costs to increase.

A shrinking job market

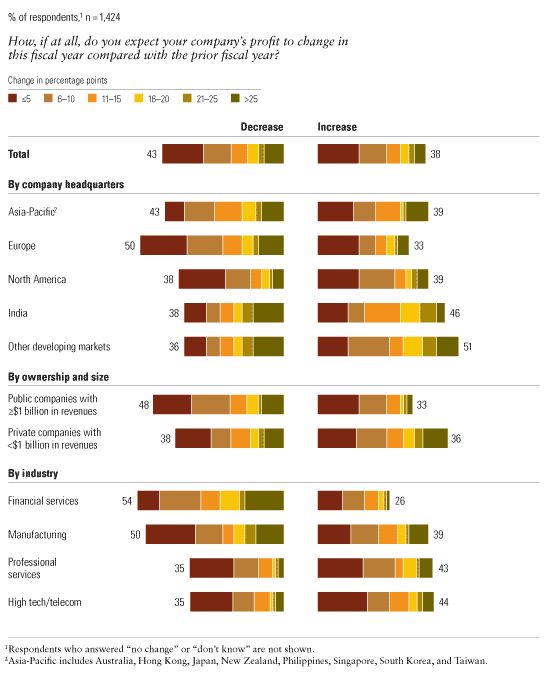

What does all this imply for corporate profits? Not bad news, many respondents say: 38 percent expect an increase this fiscal year, and 12 percent expect profits to remain stable. Executives at companies headquartered in Europe, and those in financial services, are least optimistic, with 33 percent and 26 percent, respectively, expecting an increase (Exhibit 4). Once again, smaller and private companies are likelier than others to expect profits to rise.

Some optimism on profits

As executives try to understand what the next few months will hold, they are looking mostly at the availability of credit and corporate funding and at the situation of consumers: purchasing power, debt, job losses, and overall sentiment. Yet 56 percent of respondents say they are unable to make good sales forecasts in the current situation and 30 percent say the same about customer preferences, indicating that some may find it difficult to chart a clear course.

The bigger picture isn’t pretty

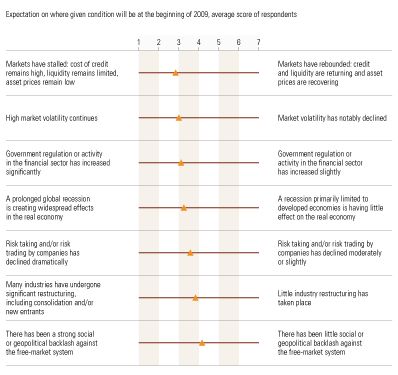

Though many individual corporations are holding their ground, executives are very gloomy about national and global economic trends. At the beginning of 2009, most expect to see a global recession, high market volatility, and financial markets still more stalled than liquid (Exhibit 5). There are startlingly few notable differences among executives in different regions or industries, or at companies of different sizes or types. Two-thirds of respondents also expect to see a decrease in their industries’ growth rates, and 54 percent expect industry consolidation, although only 7 percent expect to face competition from new entrants in their industries.

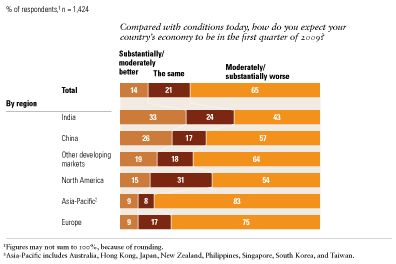

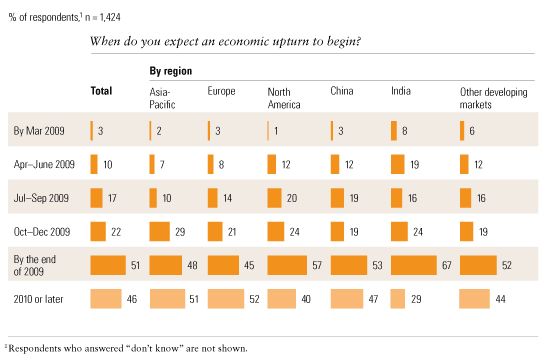

Two-thirds of executives expect their countries’ economies to be worse in the first quarter of 2009 than they are now, with some interesting regional variation (Exhibit 6). The fact that a third of North Americans think that conditions will remain the same there may indicate that some, at least, are seeing a bottom in the region. That is consistent with the finding that North Americans are the likeliest among executives in any developed region to expect an upturn sometime in 2009 (Exhibit 7).

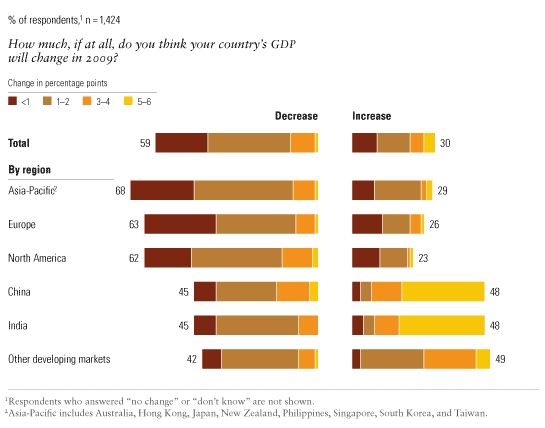

Regardless of when exactly they expect the economy to turn upward, 59 percent of executives expect the GDPs of their respective countries to decline in the next calendar year, with notable differences between developed and emerging markets in both the proportion expecting a decline and the amount of the decline they expect (Exhibit 8).

Trending badly

Dark expectations

An upturn in 2009?

Slower growth

When asked which specific indicator they’re using to indicate an upturn, the vast majority of respondents say sales or consumer sentiment, economic growth, or employment figures. But a few are using more idiosyncratic indicators, from how long lines are at taxi stands to the price of luxury items such as champagne and caviar to their own gut reactions.

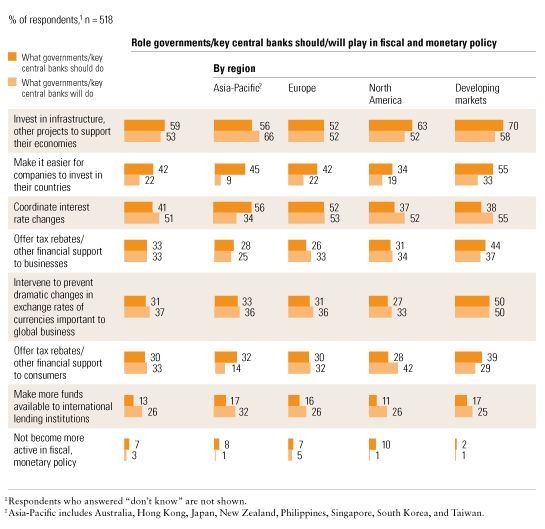

What governments should do

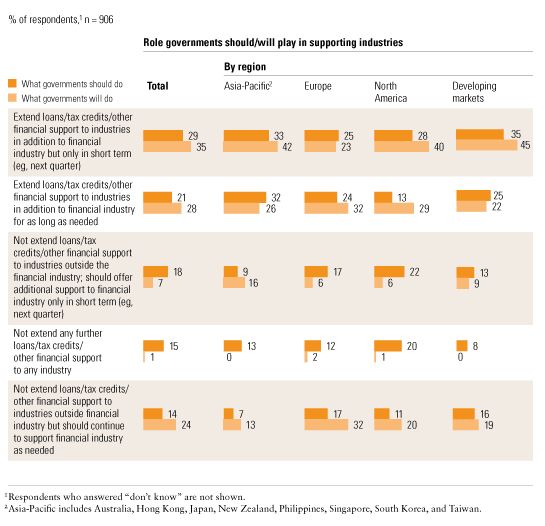

We asked respondents what governments should do—and what they expect governments will do—to quell the global economic turmoil. Executives around the world have some different recommendations for what governments should do and markedly different expectations of what they will do.

There is far more agreement, for example, that regulating existing troubled financial products should and will be the focus of new regulation (Exhibit 9) than there is on the role governments should and will play in supporting industries (Exhibit 10). The biggest differences show up in executives’ views on how governments should expand their fiscal and monetary policy compared with how they expect governments to act (Exhibit 11); they expect more purely financial action and less policy change than they think is ideal.

The focus of new regulation: troubled products

How governments can help

How to manage fiscal and monetary policy