As the global downturn continues, the world economy faces a period of lower oil prices and overall demand for energy, a welcome change for consumers after the price spikes of recent years. But unless policy makers can find ways to improve the balance between energy supply and demand, the current slackness in energy markets will last no longer than it takes for the global economy to recover. That scenario will eventually impose significant costs on consumers and businesses in the form of higher energy prices. The importance of achieving a supply–demand balance extends, of course, beyond the next few years: in the longer term, demand seems set for robust growth.

As of late April 2009, the price of oil stood at around $50 a barrel—down from a high of nearly $150 a barrel in July 2008, though many observers doubt that oil demand will rebound enough after the current economic downturn to prompt another price shock. However, research from the McKinsey Global Institute conducted in 2008 and 2009 reveals the potential for a new spike in the price of oil between 2010 and 2013. Exactly when this potential spike will occur—or if overall demand for energy will reach levels significantly above those of the pre-crisis period—depends on the length of the economic downturn.

In terms of basic market forces, it’s well known that demand for oil reacts strongly to GDP levels. Sectors such as maritime shipping, trucking, petrochemicals, and air travel not only consume petroleum products heavily but also tend to overrespond to GDP downturns. On the supply side, the longer the downturn lasts and credit markets remain tight, the more high-cost supply projects will be delayed or shelved altogether. Projects nearing completion between 2009 and 2010 will be finished, but that will not ensure sufficient supply, according to our research, since marginal projects slated for startup in 2011 and beyond will be delayed, at least temporarily.

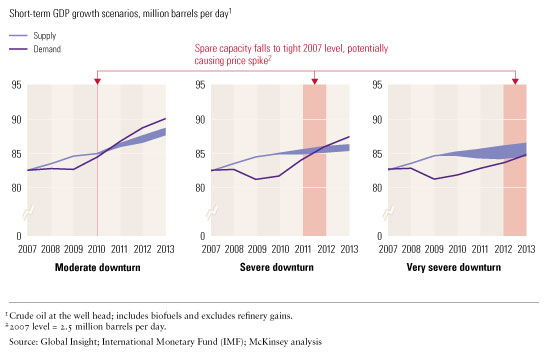

What does this mean for oil markets? For starters, the tight demand–supply balance seen at the end of 2007 could return sooner than many observers might have anticipated. A spike in the price of oil could occur as soon as 2010 under the International Monetary Fund’s (IMF) “moderate” downturn scenario, which assumes a 4.7 percent GDP gap to trend with growth falling mostly in 2008 and 2009, followed by recovery in 2010. Under a “very severe” downturn scenario (which assumes a gap to trend of 10.8 percent), the time when spare capacity returns to the tighter levels of 2007 (2.5 million barrels a day) could be delayed until 2013, causing a potential price spike (Exhibit 1).

Back to the future

Observers who doubt that a new oil shock will occur when the economy recovers refer to the period that followed the second oil crisis in the 1970s, when demand for oil grew slowly for nearly two decades. However, the substitution of other products for petroleum-based ones in, for example, power generation and heating played a key role in mitigating demand in the 1980s. There are still significant low-cost opportunities on the table to replace oil with other energy sources: an estimated 8 million barrels per day of potential to boost energy efficiency and another 8 million barrels per day available from substituting petroleum products for natural gas. It is vital that these opportunities are captured, particularly given that there is a higher share of overall energy demand in some countries and regions—most notably in China, India, and the Middle East, whose economies are still rapidly increasing their levels of petroleum consumption. There are significant political hurdles to capturing this potential, but without further action to abate growing demand, a new oil shock seems inevitable.

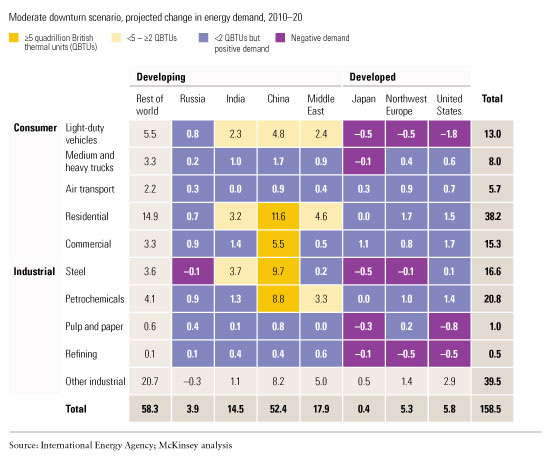

In the long term, our research suggests continued rapid growth in overall demand for energy, further boosting the importance of efficiency efforts. From 2010 to 2020, assuming a moderate GDP downturn scenario, demand for energy will grow by 2.3 percent a year, nearly a full percentage point more than projections for 2006 to 2010. More than 90 percent of this demand expansion will come from developing regions, with China, India, and the Middle East leading the way. Five sectors within China—residential and commercial buildings, steel, petrochemicals, and light vehicles—will account for more than 25 percent of global energy demand growth. India’s light-vehicle, residential-buildings, and steel sectors and the Middle East’s light-vehicle and petrochemicals sectors will be other notable contributors to the growing demand for energy (Exhibit 2).

Demand grows in developing countries

In contrast, we estimate that growth in energy demand will be virtually flat in Japan, as well as in the United States, where demand for fossil fuels will remain largely unchanged until 2020 and overall energy demand will grow at 0.4 percent per year. Europe, however, will see the rate of growth increase to around 1 percent, reflecting higher economic growth in the developing countries of Central and Eastern Europe. Several sectors in developed economies will see energy demand contract. Most notable are the light-vehicle sector, where energy efficiency regulations are leading to a dramatic slowdown in energy demand, and the pulp and paper sector, where demand is shrinking as a result of a shift from paper to digital media.

If policy makers act to head off a potential price shock—in response to a renewed imbalance in energy markets—there is considerable potential on the demand side (the focus of this research) as well as on the supply side. By 2020, we estimate that growth in demand for oil could fall by 6 million to 11 million barrels a day, which would probably balance demand and supply within this period. The available policy levers, which could be used at reasonable cost to make this happen, include incentives to shift petroleum out of boiler-fuel applications, mostly into natural gas; the removal of subsidies for petroleum products; and further incentives to raise fuel efficiency. To avoid an oil shock in a 2010 to 2013 time frame, policy makers would need to ramp up fuel-efficiency standards in developing countries rapidly while actively working to remove subsidies and create incentives for substitution.

Regulatory action to increase the productivity of all sources of energy—the output achieved for a given level of energy consumed—could abate the projected 2020 demand by between 16 and 20 percent. This could cut energy demand growth from now until 2020 by two-thirds or more. Heating and cooling buildings more efficiently, for example, presents significant opportunity for reducing energy demand, though this will require establishing and enforcing strong building standards. Developing countries represent most of the potential savings, partly because between now and 2020 they will install half or more of the capital stock that will be in place in the latter year, and the economics of better heating and cooling technologies are more attractive in new buildings than in old ones.

Lower oil prices and overall demand for energy because of the economic downturn are a temporary blessing that should not lull policy makers and businesses into a false sense of complacency. Given our projections, it is essential that they step up their efforts now to secure that energy is used in more efficient ways.